Is “Name and Shame” a Valid Way to Collect Money in the Philippines?

A smartphone screen flickers with a notification that quickly turns into a nightmare. An individual scrolls through their social media feed only to find their own face featured in a "Wanted: Scammer" post. The caption labels them a "certified buraot" or a "thief," tagging their employer, their parents, and their closest friends in the comments. What started as a private financial disagreement over a few thousand pesos has transformed into a viral campaign of humiliation.

To a frustrated creditor, this feels like the only way to get results after months of ignored messages. They believe that by bringing the private dispute into the public eye, they can shame the debtor into paying. However, in the digital age, this shortcut to collection often backfires. By hitting “post,” the creditor may unknowingly trade a civil credit dispute for a criminal record, turning a simple collection case into a high-stakes legal battle over character and privacy.

What is “Public Debt Humiliation”

In the Philippine, this term covers any digital act that publicly discloses or broadcasts a borrower’s alleged indebtedness in an embarrassing, threatening, or defamatory manner. This includes posting a debtor’s photo with insults on Facebook, tagging their social circle in group chats, sending bulk text "blasts" calling them a thief, or altering profile pictures to include derogatory labels.

This mechanism is typically utilized by:

Traditional Collection Agents by using social media platforms to pressure individuals.

Online Lending Platforms (OLPs) which are apps that scrape contact lists upon installation to harass a borrower’s references.

Peer-to-Peer “Utang Lists” that are often circulated in barangay or workplace group chats.

While "debt shaming" is not an independent crime, it violates several overlapping statutes, with cyber libel being the most severe.

Defamation in Philippine Criminal Law

The legal backbone for prosecuting debt shaming is found in the Revised Penal Code (RPC) and the Cybercrime Prevention Act.

A. Traditional Libel (Revised Penal Code, Arts. 353-362)

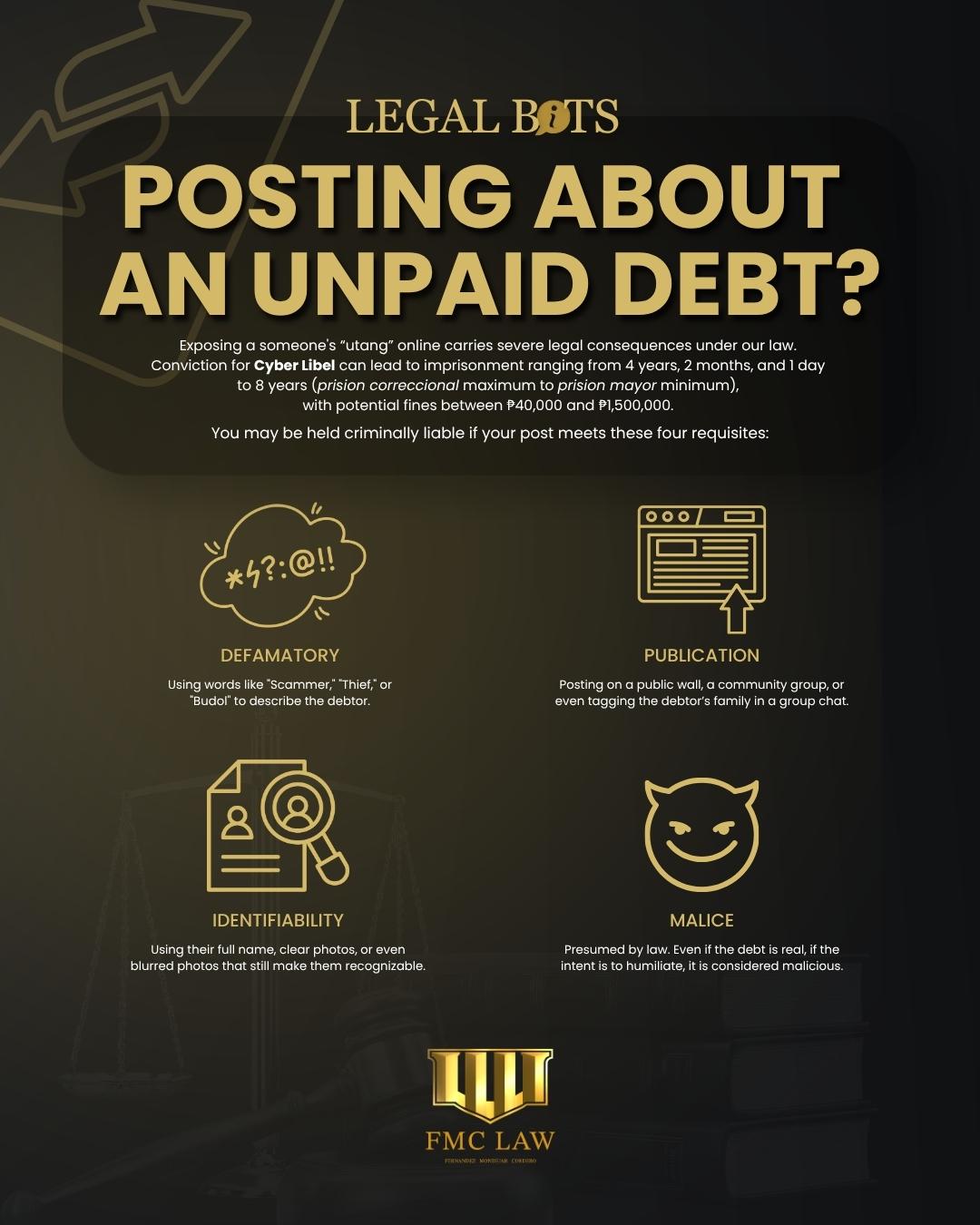

To secure a conviction, the prosecution must establish four specific elements:

Element | Description | Legal Note |

Defamatory Imputation | A discrediting statement regarding a real person. | Terms like "budol" or "scammer" suffice; specific criminal labels are not required. |

Publication | Communication of the statement to at least one third person. | Sending a shaming message to a family member in a group chat constitutes publication. |

Identifiability | The person defamed can be easily recognized. | Using a photo, a full name, or enough context to identify the person is sufficient. |

Malice | The intent to do harm (presumed by law). | Malice is presumed unless the post falls under a "privileged" category (e.g., a private court filing). |

For traditional libel, the penalty is imprisonment of 6 months and 1 day to 4 years and 2 months, plus fines.

B. Cyber Libel

Republic Act No. 10175 adopts the RPC definition but adds two significant factors:

Medium: The act is committed through information and communication technologies.

Increased Penalty: The penalty is one degree higher than traditional libel, reaching prisión correccional maximum (up to 6 years) and a fine of up to ₱1,500,000.

In Disini v. Secretary of Justice (G.R. No. 203335), the Supreme Court highlighted that the virality of the internet aggravates the injury to the victim, justifying the heavier penalty. Currently, while some courts argue for a 15-year prescriptive period, practitioners generally file cases within one year to remain cautious.

Other Laws Guarding Against Debt Shaming

Beyond libel, creditors face a gauntlet of administrative and criminal regulations designed to protect consumer privacy and dignity:

Data Privacy Act (RA 10173): Prohibits the unauthorized processing and "malicious disclosure" of personal data. Rulings by the National Privacy Commission (NPC), such as the AZG Lending case, hold that using scraped contact lists for shaming can lead to fines up to ₱5 million and criminal prosecution.

Financial Products and Services Consumer Protection Act (RA 11765): This 2022 law expressly bans the act of "publicly humiliating or harassing" a borrower. Regulatory bodies like the SEC or Bangko Sentral can revoke a lender's registration and impose daily fines for violations.

SEC Memorandum Circular 18-2019: Requires lenders to adopt "Fair Collection Policies." It strictly prohibits contacting people in a debtor's list other than guarantors or using profane language.

Unjust Vexation (Art. 287, RPC): This is often charged when the conduct is irritating or annoying but does not reach the level of full defamation.

How One Post Becomes Cyber Libel

Consider a common scenario. A collection agent posts a photo of "Juan Dela Cruz" on a public page with the text: "Do not trust this person! He is a swindler who owes ₱15,000 and refuses to pay!" Ten of Juan's friends are tagged in the post.

The Imputation: Labeling him a "swindler" suggests criminal behavior.

The Publication: Tagging friends and posting publicly ensures widespread dissemination.

The Identification: The full name and photo leave no doubt as to who is being targeted.

The Malice: Because the post is public and designed to humiliate rather than resolve the debt through court, malice is presumed.

The truth is not a complete defense. It must be published with good motives and for justifiable ends. Collecting a debt via Facebook is generally not considered a justifiable end.

Who May Be Held Criminally Liable

Liability is not limited to the person who typed the post. It can extend to:

Authors & Originators: Bloggers, vloggers, and social media managers.

Editors & Moderators: Group admins who actively screen or allow defamatory posts.

Business Managers: Operators who participated in or consented to the shaming policy.

Corporate Entities: Under RA 10175, corporations can be fined up to ₱10 million if the offense involves a corporate computer system.

Breakdown of Penalties

The consequences of a "shame post" are multi-layered and go far beyond a simple fine.

Penalty Type | Details |

Imprisonment | For Cyber Libel, the range is typically from 4 years, 2 months, and 1 day to 8 years (prision correccional maximum to prision mayor minimum) |

Fines | Courts exercise discretion but often set fines between ₱40,000 to ₱1,500,000. |

Civil Damages | Complainants can sue for moral and exemplary damages for reputational injury. |

Accessory Penalties | Suspension of the right to vote; for foreign offenders, deportation follows the completion of the prison sentence. |

Recovering What You are Owed

There are legal avenues for debt recovery that do not involve the risk of criminal prosecution.

Formal Demand Letter

The first step should always be a private, formal demand letter drafted by a professional. This creates a clear legal paper trail and often prompts payment without the need for a public confrontation.

Small Claims Court

For debts not exceeding ₱1,000,000, the Small Claims process is a fast and inexpensive way to get a court order for payment. Lawyers are not allowed to represent parties in the hearing, making it accessible for everyone.

Barangay Conciliation

If the parties live in the same city or municipality, the law requires them to go through the Lupong Tagapamayapa before filing a case in court. This is often the most effective way to reach a settlement.

Protecting Your Rights in a Digital Economy

In the Philippines, "naming and shaming" a debtor online is a legal hazard that often costs the creditor more than the debt itself. While the frustration of an unpaid loan is real, the destruction of a person’s digital reputation is an irreparable injury that the law protects fiercely.

Protecting your rights—whether as a lender or a borrower—requires a strategy that respects the rule of law. Taking justice into your own hands through digital humiliation is a move that often turns the victim into the defendant. If you are facing harassment from a lender or if you are a creditor struggling to collect through legal means, seeking a legal consultation in Iloilo or Manila is the only way to protect your interests.

Whether you need an Iloilo litigation attorney or an attorney in Manila, professional law services to resolve financial conflicts without crossing the line into criminal liability. Speak with a lawyer today to ensure your next move is a legal one.